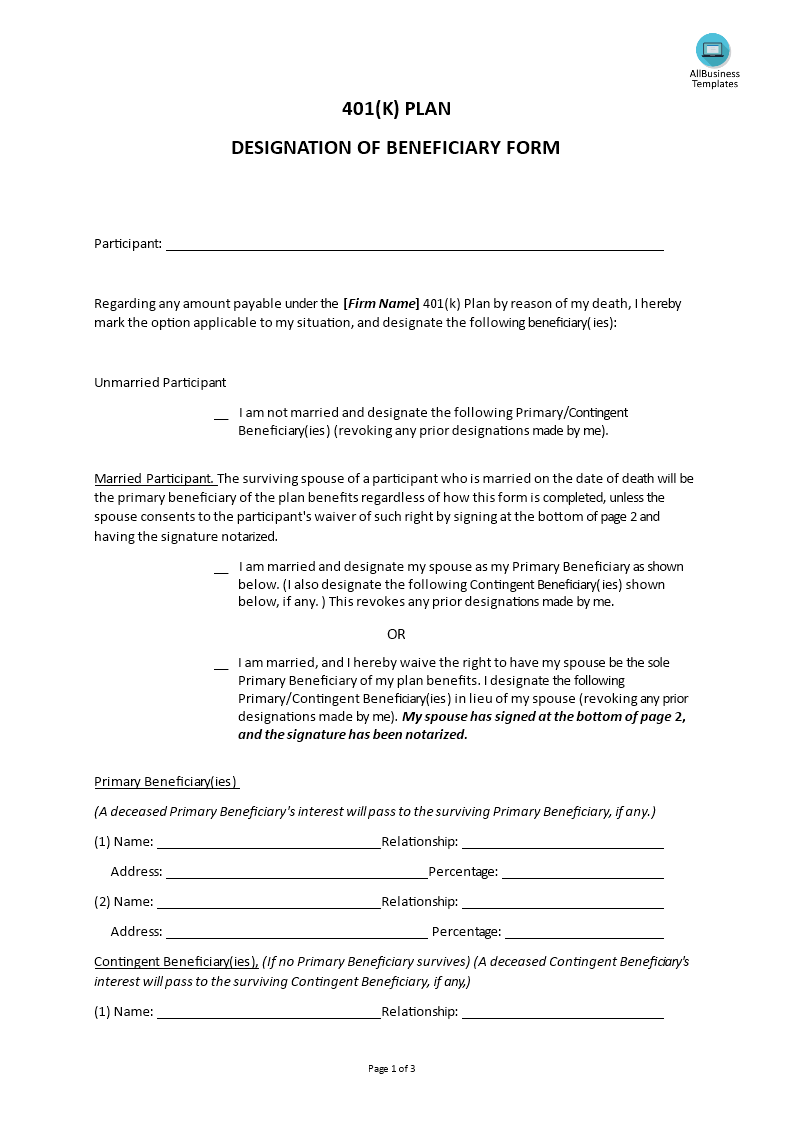

401K Aanwijzing van begunstigde

Opslaan, invullen, afdrukken, klaar!

De beste manier om een 401K Aanwijzing van begunstigde te maken? Check direct dit professionele 401K Aanwijzing van begunstigde template!

Vandaag: USD 5.99

Download nu!

Beschikbare bestandsformaten:

.docx- Gevalideerd door een professional

- 100% aanpasbaar

- Taal: English

- Digitale download (32.15 kB)

- Na betaling ontvangt u direct de download link

- We raden aan dit bestand op uw computer te downloaden.

Wettelijk Privé Notaris testament en testament

Do you need a 401K Designation of Beneficiary? Are you aware of important mistakes to avoid when drafting Beneficiary Designations? Is a spouse automatically beneficiary of a 401K?

These and more questions are answered in our document. This ready-made form for designating beneficiaries of the 401K template is well suited for any kind of personalized matter.

If you are married, and the federal law has a precondition that your spouse automatically becomes the beneficiary of your 401K or another pension plan, this is what will happen. Many people have a preferred choice to who to leave their assets to. If they choose to name a spouse, children, or other relatives as their beneficiary. If you want to leave the assets in your 401(k) plan to someone other than your spouse, he or she may need to sign a spousal consent form. Many assets pass by beneficiary designation — which is the ability to fill out a form with the financial company holding the asset and name who will inherit the asset upon your death. However, you should still fill out the beneficiary form with your spouse's name, for the record. If you want to name a beneficiary who is someone other than your spouse, your spouse must sign a waiver.

Beneficiary Designations, important mistakes to avoid

Do not take the Beneficiary Designations lightly. It is easy to make a small mistake, that can become an expensive problem with your beneficiary designations. Most people do not realize they might not fully control who inherits all their assets when they die. Many assets are passed by beneficiary designation, which is the ability to fill out a form with the financial company holding the asset and name who will inherit the asset upon your death.

However, also consider assets such as life insurance, annuities, and retirement accounts (401(k)s, IRAs, 403bs, and similar accounts) all pass by beneficiary designation. On top of this, financial firms also give you the opportunity to name beneficiaries on non-retirement accounts, which are known as TOD (transfer on death) or POD (pay on death) accounts.

While naming a beneficiary can be an easy way to ensure your loved ones will receive assets directly, beneficiary designations can also cause many problems.

It is your responsibility to make sure your beneficiary designations are properly filled out and given to the financial company — and mistakes can be costly.

Here are five essential mistakes to avoid when dealing with your beneficiary designations:

1. Not naming a beneficiary

If the owner of a retirement plan account is single when he or she dies, the assets go to the participant's designated beneficiary, no matter what his or her will states. If the participant fails to designate a beneficiary, the terms of the plan document govern the disposition of the participant's account. Many do not specifically name a beneficiary for retirement accounts or life insurance, for several reasons, such as they do not understand the importance at the moment, they take the insurance. However, if you do not name a beneficiary for life insurance or retirement accounts, then the insurer can follow their own policy where the assets will go after you die. Often, for life insurance, the funds are released to your probate estate. In such a case, the family still needs to hire a lawyer, go to court, and probate your estate to claim the proceeds.

2. Not taking tax into consideration

Any money a beneficiary receives from the inherited 401K is taxable in the year it is paid. For retirement benefits, if you are married, your spouse will most likely receive all the assets you leave behind. But, in case you are not married, you still need to name your beneficiary, otherwise, the retirement account will likely be paid to your probate estate within five years of death, which has unpleasant income tax ramifications. This causes acceleration of the deferred income tax, which must be paid earlier than would have otherwise been necessary. The 401K administrator will report the distribution to the IRS under the beneficiary's name and Social Security number, not those of the deceased participant. Distributions from a 401K are taxed in the same way as ordinary income is.

3. Naming the wrong and not updating beneficiaries over time

People close to you might change, which means the incorrect individuals are mentioned in your beneficiary designation forms. Your consideration might also change over time. Or you might make a mistake when filling in the right names. Not having names match exactly can cause delays in payouts, and in a worst-case scenario of two people with similar names, it can result in litigation.

4. Not considering special circumstances

Since not all loved ones might receive an asset directly, for example, minors (until turns 18), individuals with specials needs, or individuals with an inability to manage assets or with creditor issues, this might be something to arrange properly as well.

5. Not reviewing beneficiary designations with legal and financial advisers.

How beneficiary designations should be filled out is part of an overall financial and estate plan. It is best to involve your legal and financial advisers to determine what is best for your individual situation. Remember, beneficiary designations are created to ensure you have the ultimate say over who will get your assets when you are gone. By taking the time to thoroughly and rightly select your beneficiaries and then periodically reviewing those choices and making any necessary updates, you stay in control of your money and that is what estate planning is all about, after all.

Using our ready to use and easy to modify 401K Designation Of Beneficiary gives you more insight and time to focus on important subjects. We support you by providing this 401K Designation Of Beneficiary template, which will save you time, cost, and effort to help you arrange your legacy properly.

Download this original public notary 401K Designation Of Beneficiary MS Word template now!

Do you need more information? AllBusinessTemplates.com provides many kinds of legal and business templates in the range from IT, Environmental, Startups, Marketing, Sales, Procurement, Law, Notary, Finance, HR, Auction, Logistics, Transportation, Maintenance Services, etc. Just search on our website and have instant access to thousands of free and premium business document templates, forms, letters, reports, plans, resumes used by professionals in your industry. All business templates are easy to find, crafted by professionals, ready to use, easy to customize and intuitive.

DISCLAIMER

Hoewel all content met de grootste zorg is gecreërd, kan niets op deze pagina direct worden aangenomen als juridisch advies, noch is er een advocaat-client relatie van toepassing.

Laat een antwoord achter. Als u nog vragen of opmerkingen hebt, kunt u deze hieronder plaatsen.