Accounting Professor

Guardar, completar los espacios en blanco, imprimir, listo!

How to draft an accounting Professor? Download this Accounting Professor template now!

Formatos de archivo disponibles:

.pdf- Este documento ha sido certificado por un profesionall

- 100% personalizable

Business Negocio Resume Currículum accounting contabilidad journal diario university Universidad Research Investigación International Internacional Accounting Curriculum Vitae Currículum Contable Vitae Accounting Curriculum Vitae Samples Curriculum vitae contable muestras

How to draft a Accounting Professor that will impress? How to grab your futures employers’ attention when you are applying for a new job? Download this Accounting Professor template now!

There are a few basic requirements for a Resume, for example, the resume should contain the following:

This Accounting Professor template will grab your future employer its attention. After downloading and filling in the blanks, you can customize every detail and appearance of your resume and finish.

In order to achieve this, you just have to be a little more creative and follow the local business conventions. Also bright up your past jobs and duties performed. Often they are looking for someone who wants to learn and who has transferable skills like:

- Leadership skills;

- Can do-will do mentality;

- Ability to communicate;

- Ability to multi-task;

- Hard work ethics;

- Creativity;

- Problem-solving ability.

- brief, preferably one page in length;

- clean, error-free, and easy to read;

- structured and written to highlight your strengths;

- immediately clear about your name and the position you are seeking.

Completing your Accounting Professor has never been easier, and will be finished within in minutes... Download it now!

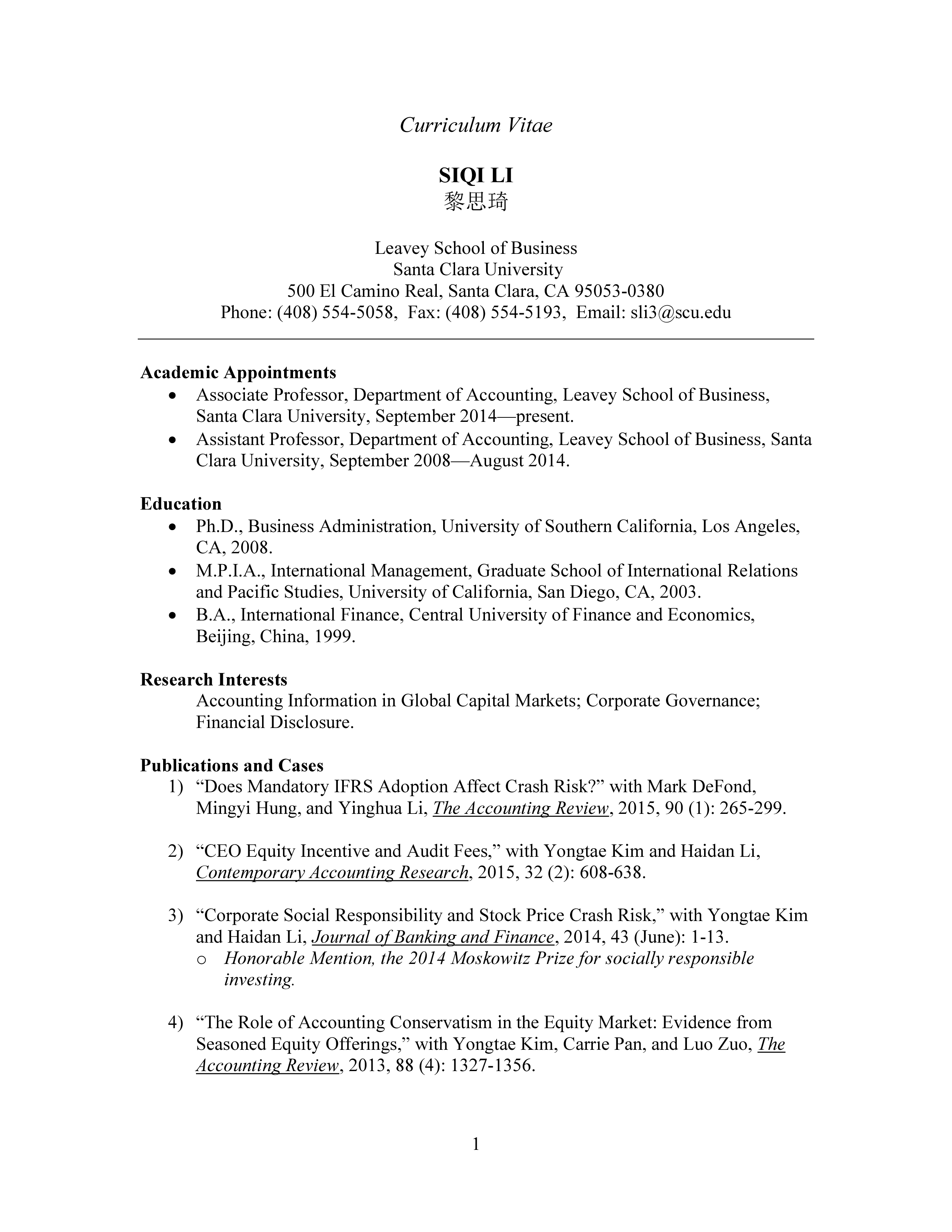

(August 2012) “Mandatory IFRS Adoption in the EU and Cross-Border Intra-Industry Information Transfers” o Keio University (June 2010) Sogang University (June 2010) University of Hong Kong (June 2010) Shanghai University of Finance and Economics (May 2010) Central University of Finance and Economics (March 2010) Hong Kong Polytechnic University (February 2010) Santa Clara University (December 2009) “The Role of Accounting Conservatism in the Equity Market: Evidence from Seasoned Equity Offerings” o 2011 FMA Annual Meeting, Denver (October 2011) 2011 AAA Annual Meeting, Denver (August 2011) Santa Clara University (April 2011) “Has the Widespread Adoption of IFRS Reduced US Firms’ Ability to Attract Foreign Capital ” o FARS Midyear Meeting, Chicago (January 2012) National University of Singapore (May 2011) Santa Clara University (May 2011) Texas A M University (April 2011) “CEO Equity Incentive and Audit Fees” o 2011 AAA Annual Meeting, Denver (August 2011) AAA Western Meeting, San Diego (April 2011) “The Impact of Mandatory IFRS Adoption on Foreign Mutual Fund Ownership: The Role of Comparability” o University of Texas, Austin (January 2011) Tilburg University (December 2010) Central University of Finance and Economics (September 2010) 2010 AAA Annual Meeting, San Francisco (August 2010) Stanford Summer Camp (August 2009) National University of Singapore (July 2009) University of Southern California (July 2009) University of Oregon (July 2009) Santa Clara University (July 2009) University of Maryland (2009) Northwestern University (March 2009) “Does Eliminating 20-F Reconciliation from IFRS to U.S. GAAP Have Capital Market Consequences ” o International Risk Management Conference, Amsterdam (June 2011) 2010 AAA Annual Meeting, San Francisco (August 2010) FARS Midyear Meeting, San Diego (January 2010) “Large Creditors and Corporate Governance: The Case of Chinese Banks” o 2011 Journal of International Accounting Research Conference (June 2011) “Does Mandatory Adoption

DESCARGO DE RESPONSABILIDAD

Nada en este sitio se considerará asesoramiento legal y no se establece una relación abogado-cliente.

Deja una respuesta. Si tiene preguntas o comentarios, puede colocarlos a continuación.