HTML Preview Real Estate Settlement Statement page number 1.

Previous editions are obsolete

form HUD-1 (3/86)

ref Handbook 4305.2

Page 1 of 2

U.S. Department of Housing

and Urban Development

(expires 9/30/2006)

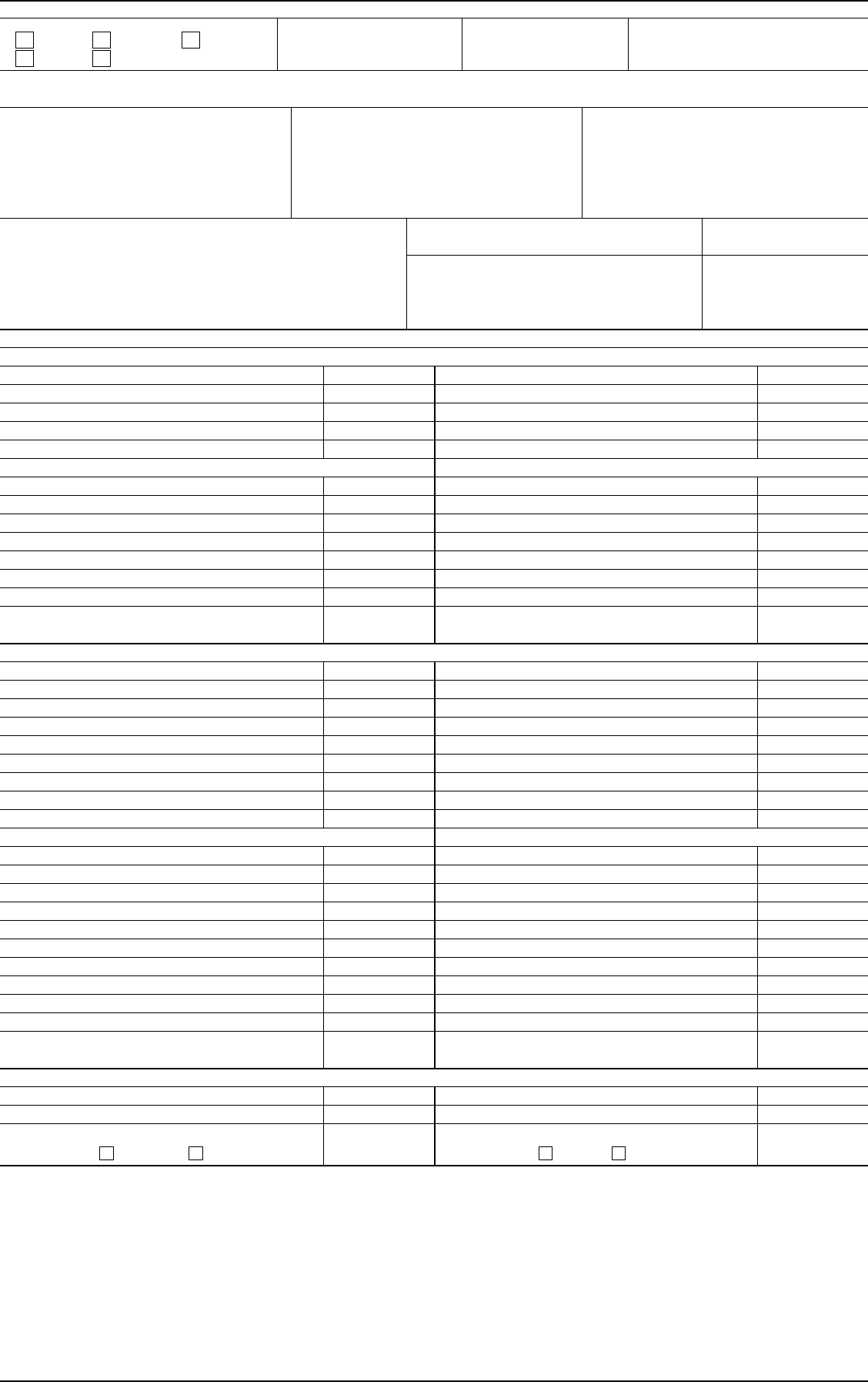

A. Settlement Statement

OMB Approval No. 2502-0265

C. Note: This form is furnished to give you a statement of actual settlement costs. Amounts paid to and by the settlement agent are shown. Items marked

“(p.o.c.)” were paid outside the closing; they are shown here for informational purposes and are not included in the totals.

D. Name & Address of Borrower: E. Name & Address of Seller: F. Name & Address of Lender:

G. Property Location: H. Settlement Agent:

Place of Settlement: I. Settlement Date:

J. Summary of Borrower's Transaction K. Summary of Seller's Transaction

100. Gross Amount Due From Borrower 400. Gross Amount Due To Seller

101. Contract sales price 401. Contract sales price

102. Personal property 402. Personal property

103. Settlement charges to borrower (line 1400) 403.

104. 404.

105. 405.

Adjustments for items paid by seller in advance Adjustments for items paid by seller in advance

106. City/town taxes to 406. City/town taxes to

107. County taxes to 407. County taxes to

108. Assessments to 408. Assessments to

109. 409.

110. 410.

111. 411.

112. 412.

120. Gross Amount Due From Borrower 420. Gross Amount Due To Seller

200. Amounts Paid By Or In Behalf Of Borrower 500. Reductions In Amount Due To Seller

201. Deposit or earnest money 501. Excess deposit (see instructions)

202. Principal amount of new loan(s) 502. Settlement charges to seller (line 1400)

203. Existing loan(s) taken subject to 503. Existing loan(s) taken subject to

204. 504. Payoff of first mortgage loan

205. 505. Payoff of second mortgage loan

206. 506.

207. 507.

208. 508.

209. 509.

Adjustments for items unpaid by seller Adjustments for items unpaid by seller

210. City/town taxes to 510. City/town taxes to

211. County taxes to 511. County taxes to

212. Assessments to 512. Assessments to

213. 513.

214. 514.

215. 515.

216. 516.

217. 517.

218. 518.

219. 519.

220. Total Paid By/For Borrower 520. Total Reduction Amount Due Seller

300. Cash At Settlement From/To Borrower 600. Cash At Settlement To/From Seller

301. Gross Amount due from borrower (line 120) 601. Gross amount due to seller (line 420)

302. Less amounts paid by/for borrower (line 220) ( ) 602. Less reductions in amt. due seller (line 520) ( )

303. Cash From To Borrower 603. Cash To From Seller

6. File Number: 7. Loan Number: 8. Mortgage Insurance Case Number:

1.

FHA 2. FmHA 3. Conv. Unins.

4. VA 5. Conv. Ins.

B. Type of Loan

Section 4(a) of RESPA mandates that HUD develop and prescribe this

standard form to be used at the time of loan settlement to provide full

disclosure of all charges imposed upon the borrower and seller. These are

third party disclosures that are designed to provide the borrower with

pertinent information during the settlement process in order to be a better

shopper.

The Public Reporting Burden for this collection of information is estimated

to average one hour per response, including the time for reviewing instruc-

tions, searching existing data sources, gathering and maintaining the data

needed, and completing and reviewing the collection of information.

This agency may not collect this information, and you are not required to

complete this form, unless it displays a currently valid OMB control number.

The information requested does not lend itself to confidentiality.

Section 5 of the Real Estate Settlement Procedures Act (RESPA) requires

the following: • HUD must develop a Special Information Booklet to help

persons borrowing money to finance the purchase of residential real estate

to better understand the nature and costs of real estate settlement services;

• Each lender must provide the booklet to all applicants from whom it

receives or for whom it prepares a written application to borrow money to

finance the purchase of residential real estate; • Lenders must prepare and

distribute with the Booklet a Good Faith Estimate of the settlement costs

that the borrower is likely to incur in connection with the settlement. These

disclosures are manadatory.